Image by Gerd Altmann from Pixabay.

Image by Gerd Altmann from Pixabay.

The economic crisis in Cuba: Its causes and effects on migration

During the sessions of Cuba’s National Assembly in July 2024, a senior official acknowledged a significant decline in the island’s population. According to official figures, at the end of the year, the country had approximately 9.7 million inhabitants. However, these estimates should be taken with caution, as the last National Population and Housing Census was conducted in 2012, and the 2022 census has yet to be finalized, introducing significant margins of error into current statistics.

Some experts argue that the demographic outlook is even more critical.(1) For example, Albizu-Campos estimates that by mid-2024, the total population will have fallen below 9 million. Regardless of the reference number, there is broad consensus—among both analysts and citizens—on two fundamental aspects: the country is experiencing the most significant migratory exodus since the 20th century, and the impact of this phenomenon on the economy and social fabric is profound, although its medium- and long-term effects remain uncertain.

In this context, various voices—including political actors, analysts, and authorities—have attributed the exodus primarily to the effects of the sanctions imposed by the United States. This narrative establishes a direct causal relationship between the coercive measures and the internal economic crisis, while dismissing or minimizing the influence of other structural factors.

However, a rigorous review of analyses by renowned economists indicates that the diagnosis has evolved into a broader consensus: the current crisis is likely the most severe since 1959. This assessment is based on multiple dimensions, including the sustained contraction of production, the partial collapse of public services, the deterioration of wage purchasing power, the rise of informality, and an increase in inequality.

In this sense, it is reductionist to attribute the situation solely to external factors, particularly U.S. sanctions, although these have undoubtedly exacerbated domestic vulnerabilities. Ignoring the responsibility of domestic economic policy—marked by reformist inertia, state control over productive activity, and limited openness to the private sector—hinders a comprehensive understanding of the problem and restricts the ability to formulate effective responses.

Manifestations of the Crisis

Although some traditional indicators suggest that the current crisis is less severe than the one experienced in the early 1990s, it is difficult to underestimate the gravity of the situation. By 2024, GDP was more than 10% below 2018 levels. While this contraction is smaller than the collapse of the early 1990s—when the economy shrank by almost 40% in just four years—the current starting point is considerably more precarious.

In 1990, the country had a robust network of social services, relatively low levels of inequality, and a standard of living that, in retrospect, was higher than in subsequent decades. By 2019, after almost 30 years of stagnation, unfinished reforms, and growing social insecurity, many families still had not been able to recover their previous well-being. The accumulated deterioration of key sectors such as health and education, coupled with the collapse of the rationing system, which has lost coverage and reliability, creates a more vulnerable environment in the face of any shock.

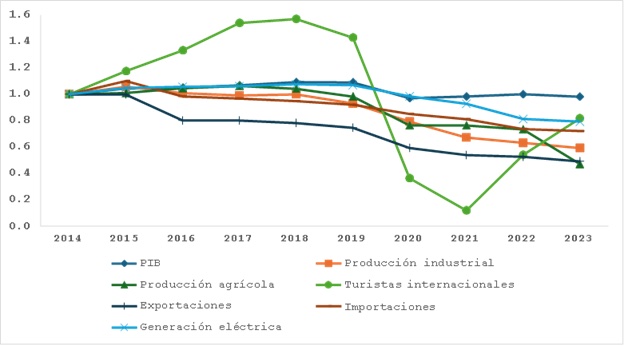

Other indicators more clearly demonstrate the severity of the current crisis. The industrial production index (1989 = 100) stood at just 38.6 in 2023, and the sugar sector—for decades the country’s productive backbone—dropped to an alarming 4.6. In agriculture, root and vegetable production levels are less than half of what they were a decade ago. International tourism and electricity generation also exhibit significant contractions (Figure 1).

The external front displays a similar dynamic. Exports have halved compared to their 2013 peak, while imports have declined by 37%, with even smaller volumes in physical terms due to the sustained increase in international prices.

Current account surpluses shifted to deficits beginning in 2020, and after successfully renegotiating its external debt with the Paris Club in 2015, Cuba once again suspended payments to creditors and suppliers.(3) Foreign investment has consistently fallen short of official targets, and remittances have also displayed a downward trend, with variations depending on the source and estimation methods.

These results indicate that economic stagnation began before the COVID-19 pandemic and even prior to 2019. With the exception of a temporary rebound in tourism during certain years, the economy has not exhibited a pattern of robust growth for over a decade.

These results indicate that economic stagnation began before the COVID-19 pandemic and even prior to 2019. With the exception of a temporary rebound in tourism during certain years, the economy has not exhibited a pattern of robust growth for over a decade.

Real GDP is below the level reached in 2014, effectively losing a decade of economic progress. Additionally, it is striking that the decline in GDP appears moderate compared to the very sharp declines observed in other key indicators. This may reflect methodological statistical limitations in its calculation.

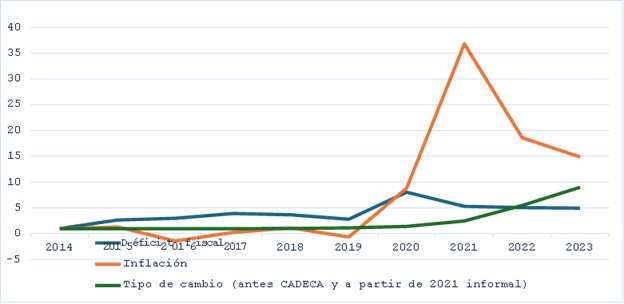

Compounding this situation are the worsening macroeconomic imbalances (Figure 2). Inflation has sharply rebounded since 2021, with official rates of +77% in 2021, +39% in 2022, and +31% in 2023, although various independent estimates suggest that actual levels have reached triple-digit figures.

The Cuban peso (CUP) has experienced a dramatic depreciation, plummeting from 40 to the dollar in January 2021 to 350 in April 2025, reflecting a loss of 88% of its value. The immediate causes include high fiscal deficits, a prolonged contraction in foreign currency revenues, and a considerably reduced supply of goods and services.

In an economy like Cuba’s—highly dependent on foreign currency and possessing structural rigidities in production—the sustained application of expansionary fiscal policies, without a clear source of external financing or a corresponding increase in production, tends to fuel inflationary processes and cause severe currency depreciations. Authorities have projected a fiscal deficit exceeding 10% of GDP by 2025, an unsustainable figure in the current context.

In an economy like Cuba’s—highly dependent on foreign currency and possessing structural rigidities in production—the sustained application of expansionary fiscal policies, without a clear source of external financing or a corresponding increase in production, tends to fuel inflationary processes and cause severe currency depreciations. Authorities have projected a fiscal deficit exceeding 10% of GDP by 2025, an unsustainable figure in the current context.

Although the economy was already experiencing sluggishness, the current situation is marked by persistent instability and ongoing deterioration. This scenario has negatively impacted key social indicators, which had already shown signs of decline after decades of restrictions. In recent years, however, the decline has alarmingly deepened, and its effects on social structures are becoming increasingly visible.

The figures above indicate a significant and prolonged contraction in nearly all relevant economic indicators, showing a high degree of synchronization among them. This dynamic suggests that the underlying causes are more structural than temporary and transcend the immediate effects of the shocks—whether internal or external—experienced in recent years.

The Failures of the Economic System

As a centrally planned economy, Cuba suffers from a series of structural deficiencies that have become entrenched over time, and the various rounds of reforms—generally limited, gradual, and inconsistent—have failed to significantly correct these issues. Although some of these deficiencies were identified as aspects to be modified in the transformation program launched by Raúl Castro, little progress has been made.

Among the most persistent problems are the limited depth of markets or their absence in key segments such as inputs, foreign exchange, and capital markets. At the same time, a centralized allocative-administrative planning system is maintained, accompanied by typical elements like a lack of competition among state-owned enterprises, pricing misaligned with real costs, and soft financial constraints that perpetuate inefficiency.(7) In Cuba, the prevailing retrograde view fails to conceive of the market as a coordination mechanism within more general modern planning. They are substitutes, not complements.

A dynamic economy requires functional mechanisms for business entry and exit, which allow resources to be reallocated toward more productive uses. Entry promotes competition, innovation, and efficiency; exit removes obsolete structures and frees up production factors for higher value-added sectors. This cycle is fundamental to maintaining aggregate productivity and the adaptability of any economic system.

In the Cuban case, this mechanism operates minimally. Although systematic data to measure these processes is lacking, it is reasonable to assume that business entry and exit are more active in the private sector, which operates under much more flexible rules and is exposed to greater risks. However, its potential has been constrained by regulations that limit authorized sectors, hinder business growth, and restrict access to productive inputs, including land, financing, and infrastructure.

These limitations are compounded by perverse incentives stemming from an environment dominated by state-bureaucratic ownership. The disconnect between workers’ or managers’ income (salaries, bonuses) and the companies’ actual results undermines any logic of efficiency or continuous improvement.

State-owned enterprises typically operate slowly and lack adequate market signals—such as real prices or effective competition—demonstrating minimal capacity for adjustment. Similarly, planners do not possess effective tools to address imbalances, partly due to institutional fragmentation and the presence of parallel structures, such as the military business system, which operates under different rules than the rest of the civilian apparatus.

A distinctive feature of the Cuban model is the “structural aversion” to exports. This phenomenon, identified in similar models, arises from both the state monopoly on foreign trade and the design of the production system itself.

Exports are typically managed by Foreign Trade Entities (ECE), rather than by producing companies, which diminishes incentives to respond to international demand. The price ultimately received by producers is generally detached from the actual export price, isolating companies from the global market.

These state-owned enterprises (STEs) operate as monopolies within each sector, subordinated to ministries or state agencies. The disconnect between external and domestic prices is worsened by the lack of a transparent and unified exchange rate system, which hinders the establishment of clear equivalencies between foreign currency earnings and their equivalent in national currency. Prices—for both foreign and domestic trade—are determined centrally. This distorts their role as signals of scarcity and value.

Such institutional design has led to weak export dynamism and a high dependence on imports, resulting in a chronic structural imbalance in the external sector. This deficit can only be temporarily offset through external debt or special trade conditions—such as preferential prices or payment facilities—which, while alleviating short-term pressures, tend to undermine long-term competitiveness. Instead of encouraging efficiency, these conditions reinforce the disconnection of the productive apparatus from the demands of international markets.

Finally, it is essential to acknowledge that the challenges of integrating into the global market are also influenced by external factors, such as the sanctions regime imposed by the United States. Various studies document the adverse effects of these measures on Cuba’s foreign trade and its international integration pattern.

However, limiting the analysis of the crisis to the effects of the sanctions overlooks the internal operational issues that clarify much of the productive inertia, the restrictions on private sector growth, and the country’s weak export capacity.

La crisis económica en Cuba: Sus causas y efectos en la migración

Recent Shocks

As argued above, the current economic crisis in Cuba results from a complex network of deep structural factors. However, its severity and rate of deterioration cannot be understood without considering the cumulative effect of several negative external shocks that have occurred over the last decade. These events, while distinct in nature, have interacted synergistically with the weaknesses of the economic model, amplifying their effects and creating what can be described as a perfect storm.

One of the most significant shocks has been the economic crisis in Venezuela, whose prolonged recession drastically reduced its capacity to export oil and sustain bilateral cooperation with Cuba. The dissolution of the joint venture that operated the Cienfuegos refinery (CUPET-PDVSA), the drop in fuel shipments, along with some occasional recoveries, and the lower demand for medical services generated a substantial increase in foreign currency expenditures for energy imports. This raised production costs, reduced energy availability, and necessitated forced adjustments in domestic supply.

Second, the loss of key markets for medical services due to the closure of contracts with Brazil (November 2018), Ecuador, and Bolivia (both in November 2019) resulted in a significant reduction in export revenues from professional services, one of the country’s main sources of foreign currency.

Additionally, the new sanctions imposed during Donald Trump’s first administration reinforced the existing sanctions framework and broadened its scope.

Among the most significant measures are the partial closure of the U.S. embassy in Havana, the suspension of regular flights to inland provinces, the elimination of individual travel by Americans under the People-to-People category, the revocation of Western Union’s license, and the activation of Title III of the Helms-Burton Act. These actions affected multiple channels: a reduction in travelers from the United States, a drop in remittances, higher financial transaction costs, and a chilling effect on foreign investment.

The COVID-19 pandemic represented another severe external shock, albeit a global one. Border closures and the widespread contraction of global economic activity caused a sharp drop of more than 90% in international tourist arrivals.

Additionally, international trade costs increased while remittances fell due to the loss of income from migrants abroad. Supply chains were also disrupted, affecting the availability of essential goods.

The cumulative impact of these shocks—spread between 2016 and 2022—is challenging to quantify precisely, but preliminary studies suggest that losses total several billion dollars. These losses include:

- Decreased exports (due to the loss of markets for medical services, generic medicines, petroleum products, and tourism).

- Rising imports, particularly of fuels.

- Fewer personal transfers resulted from a drop in remittances.

- Rising financial and logistical costs of foreign trade.

In addition to these exogenous shocks, the impact of recent extreme events is notable, including natural disasters such as Hurricanes Matthew (2016), Irma (2017), Ida (2021), Ian (2022), and Rafael, Oscar, and Helene (2024), as well as major technological accidents like the fire at the Matanzas supertanker base, the Saratoga Hotel explosion, and the repeated collapses of the National Electric Power System (four total blackouts between October 2024 and March 2025).

While these events explain part of the recent deterioration, it would be a mistake to attribute the worsening external environment solely to the tightening of US sanctions. The data and facts show that the Cuban economy has faced multiple successive shocks. Their consequences have been even more devastating due to accumulated structural weaknesses.

The “development” model?

The economic debacle of the early 1990s marked the collapse of a development model built on very favorable external relations—especially with the Soviet Union and the European socialist bloc—relations that disappeared in a short period. It is worth noting that the tightening of the international environment began before the formal collapse of socialism in Eastern Europe and the USSR. From 1986 to 1989, Cuban GDP growth was virtually zero, foreshadowing the restrictions to come.

Faced with the crisis of the so-called Special Period, the Cuban government promoted a series of partial reforms that, while not constituting a structural transformation of the economic model, did give rise to a new growth model. This model was based on generating foreign currency income from four pillars: international tourism, remittances, the biopharmaceutical industry, and, later, the export of medical services.

Additionally, there were niches of foreign direct investment (FDI) in sectors such as rum, tobacco, and nickel. However, other strategic sectors—such as the sugar agroindustry—experienced a prolonged decline from which they have not recovered.

Despite its contribution to external revenues, this model presented structural limitations from the beginning. Many of these activities—such as exported medicine or ties with Venezuela—depended on preferential external relations rather than competitive access to international markets.

Furthermore, the domestic linkage capacity of these sectors has always been limited. For example, medical services, mining, and biopharmaceuticals have not generated significant multiplier effects on the national productive fabric.

Internally, the model was based on large state-owned enterprises operating as quasi-monopolies within a highly distorted price environment. Foreign investment was directed almost exclusively toward state-owned enterprises or joint ventures, lacking clear incentives for efficiency or significant openness to competition.

For its part, the private sector faced regulatory limits that restricted its sectoral scope, accumulation capacity, and connection to national and international value chains. This hindered foreign currency flows generated externally (tourism, remittances, exports) from being translated into a national development strategy centered on import substitution or a robust expansion of the productive apparatus. Opportunities in simple consumer goods and agricultural production were largely squandered.

As a result, the Cuban economy remained trapped in a growth model characterized by low technological content, limited domestic value-added generation, and high income elasticity of imports—that is, a pattern in which GDP increases lead to greater demand for imported goods, rather than enhancing domestic production.

Since the mid-2000s, the weaknesses of this model became increasingly evident. The prolonged Venezuelan crisis, along with political changes in Latin American governments, reduced or eliminated many of the special agreements that supported the export of medical services and medicines.

At the same time, remittances began to weaken due to both structural and political reasons: hostility from sectors of the diaspora, restrictions imposed by the United States, and generational changes in ties with the island.

International tourism, for its part, is experiencing a period of stagnation due to long-term factors such as poor quality of services, lack of connectivity, and obsolete infrastructure, along with questionable policy decisions.(9)

For more than a decade, the country has heavily invested in constructing luxury hotels—many of them in Havana—despite the lack of real demand for these segments. This has led to very low occupancy rates, low profitability, and increasing pressure on scarce financial resources. Additionally, the limited coordination of tourism with domestic suppliers reduces its spillover capacity to other sectors.

The confluence of these trends—falling exports, weakening remittances, a decline in tourism, limited attraction of foreign investment, and a stagnant productive system—has resulted in a severe contraction in foreign exchange earnings at a time when the country is also grappling with increasing external debt and a deteriorating risk profile.

The model has proven incapable of generating internal adjustment mechanisms, and the economy has reached this point with minimal reserves of physical, organizational, and political capital to confront the scale of the crisis.

Therefore, we are facing not merely a prolonged recession or a series of temporary challenges, but rather the exhaustion of a development model that never fully consolidated.

The most adverse external conditions have accelerated this deterioration, but the root of the problem lies in the absence of coherent and sustained structural reforms that would enable a transition to a more diversified, productive, and resilient economy.

Final Reflections

Cuba has operated for years in a “permanent emergency mode,” where economic decisions do not align with development strategies, but instead follow the logic of containment and survival. This situation has limited the State and the productive sector’s ability to adapt to internal and external changes, leading to a progressive deterioration of living conditions.

The previous discussion has highlighted that the economic crisis affecting Cuba since at least 2019 has multiple causes. It is not an isolated phenomenon, nor a simple consequence of external sanctions. On the contrary, the current crisis results from the confluence of structural factors—specific to the centrally planned economic model—along with a series of negative external shocks that have occurred successively in recent years.

In addition, there is a limited institutional response characterized by conservative attitudes towards reforms and a weak state that diminishes the ability to diagnose, implement, and rectify public policies. Some recent decisions, such as the failed monetary “Reordering” of 2021, not only failed to resolve the problems they aimed to address, but also deepened macroeconomic imbalances and exacerbated social tensions.

However, the effects of this crisis are not solely reflected in economic statistics. One of its most dramatic aspects has been the mass exodus of the population, representing the largest migratory flow since the mid-20th century.

While economic deterioration is the primary driver, it is not the sole factor that explains the decision to emigrate. In recent years, conditions have developed that have facilitated and encouraged leaving the country.(10)

First, access to foreign nationalities, especially Spanish, has expanded through laws such as the Historical Memory Law (2007) and the more recent Democratic Memory Law (2022), allowing tens of thousands of Cubans to obtain European citizenship.

Second, many Latin American countries—such as Ecuador, Guyana, and Nicaragua—have established visa-free regimes or simplified entry procedures for Cuban citizens. This has created migration corridors that subsequently extend to the United States.

On the other hand, at the domestic level, Decree-Law 302 of 2013 eased immigration regulations, removing the requirement for an official exit permit and extending the period of stay abroad without risking legal residency. This change greatly enhanced the international mobility of Cubans and supported more flexible, family-oriented migration strategies.

Finally, the sociopolitical context has also changed. New generations of Cubans show a different relationship with the revolutionary project: they are less identified with its symbols, narratives, and promises, and more connected to global references, expectations of personal autonomy, and demands for freedom of movement and life choices. This cultural and identity shift lowers the subjective costs of emigrating while eroding the symbolic legitimacy of the current system.

Overall, the outlook that Cuba faces is not merely that of a cyclical crisis. It reflects the exhaustion of an economic, political, and social model that has been unable to renew itself in response to a changing environment or to provide prospects for prosperity and participation to broad sectors of society.

Mass migration, in this context, serves as both a safety valve and a sign of rupture: it highlights the failure of the system to retain the talent and energy of its population and indicates the emergence of a new type of citizenry that is more mobile, disconnected, and demanding.

Any sustainable solution to this crisis will require more than just palliative measures. It will necessitate a profound review of the current model, centered on genuine economic openness, institutional strengthening, and reconnection between the country and its citizens—both on and off the island. Otherwise, the emigration of human capital and the degradation of the social fabric will persist, further diminishing the prospects for recovery.